Let’s work through the University of Connecticut’s intellectual property practice on disclosure and ownership of inventions. We will start in the middle, with a disclosure form–much like a university inventor might do.

UConn has an “Innovation Alert” web “portal” that can be used for “pre-disclosure”:

Inventors are invited to disclose before they disclose. Something about this smacks of a failure of language. One might think that this “pre-disclosure” starts the 60-day clock ticking for UConn to report a pre-disclosed invention to a federal research sponsor. I expect the university administrators who chucked up this idea will argue that this cannot be an invention disclosure because it has “pre-” right there in its name. They fail to understand that an instrument is what it does, not how it is labeled.

What is to be pre-disclosed is variously called a “big idea,” “new idea,” an “innovation,” or an “invention.” Apparently in pre-disclosure, UConn administrators cannot focus on any one thing. “Big idea” is cartoonish condescension; “new idea” is nonsense, because ideas don’t have much to do with invention, and the focus is invention not, say, business ideas in general; “innovation” is pretentious because innovation is something adopted by a group as new, a change in the established order as it were, not merely something new in one’s head or lab; and “invention” is the putative target of an “invention” disclosure form–but the “Innovation Alert” portal makes a hash out of that by inviting disclosures of stuff that isn’t inventive (in the patentable sense).

The actual focus of the disclosure should be a patentable invention–one that’s new, useful, and not obvious. How difficult is that to communicate? Furthermore, the university’s scope of claim to ownership is restricted (we will get to this later), but here the offer is to evaluate any “big idea, new idea, innovation, invention” regardless of the university’s ownership position. Big-hearted, if true.

The Innovation Alert makes more hash of the process of “pre-disclosure” by inviting inventors to provide a 50-word/600-character description of the invention. This description, the Innovation Alert insists, will “help us determine if your new idea may have a commercial application and warrants filing an Invention Disclosure.” Now what happens if the university does not have an ownership claim on a pre-disclosed invention? Has that invention then been publicly disclosed? One might think that there would be some notice on the pre-disclosure that the university will treat all “big ideas” from its apparently bouncy, fluffy inventors (with “big ideas”) as confidential information. But no, not to be.

Finally, the university purports to be able to divine from a 50-word description whether the big/new/innovative/inventive idea “may have” a “commercial application.” If so, the implication is, one might have to file an “actual” invention disclosure form. This bit is multiply silly. First, almost anything “may have” a commercial application. Second, “commercial application” is senselessly broad–is the meaning that a company might use the big/new/innovative/inventive idea or that some company might want to make a product based on the idea? And why limit the review to what a company in the business of selling (“commercial”) might want? Why not consider the research community, or the general public, or nonprofit organizations? Third, the point of an invention disclosure is to report any patentable invention, not merely the ones that some administrator decides “may have” a “commercial application.” Research sponsors in particular don’t give a rat’s ass what a university bureaucrat might conclude from a 50-word summary. They expect a report of everything that’s considered patentable. “May be patentable” is on topic. “May have commercial application” is goofball.

Of course, since the Innovation Alert is directed to a university unit that calls itself “Technology Commercialization Services,” perhaps it is to be expected that the thing of greatest import is whether there is something to be “commercialized” that can be called “technology” and not whether a patentable invention has been made that requires administrative attention to sort out, say, reporting and licensing obligations to research sponsors. Here’s TCS’s “mission”:

The mission of Technology Commercialization Services is to expedite and facilitate the transformation of UConn discoveries into products and services that benefit patients, industry and society.

The mission is to license patents on research inventions for commercial development, likely using exclusive licenses. The tag that doing so to “benefit patients, industry and society” is unreadable. The implication is that some products and services might not benefit patients, industry and society, but TCS will make sure that the products and services that result from its “transformation” will. Silly emptiness. We might also ask whether TCS does indeed “expedite” anything. How would one show that industry has gotten access to research results more expeditiously as a result of TCS activity than industry would have otherwise? We might ask, too, for an accounting of TCS’s use of exclusive licenses, whether TCS includes price controls or pro-competitive provisions in its licensing agreements, and how TCS accomodates innovation pathways that do not go through patent monopolies–pathways such as open innovation, standards, cumulative technologies, and insertion of research work into existing product bases.

The “Innovation Alert” portal creates its own confusion. It’s another instance of “Pigpen” administration, in which administrators bring their own cloud of dirt-filled thinking with them wherever they go. Tell us your “big idea” and we will tell you whether you should have bothered telling us anything. Why not drive right at what matters–inventions that are or may be patentable?

Let’s turn then to the “actual” invention disclosure form provided by UConn. In particular, let’s consider disclosure of inventions made with federal support, defined by Bayh-Dole as “subject inventions.” Universities give out bad advice about what constitutes a subject invention. The UConn invention disclosure form is available here. (Warning: downloads a Word file). Here’s what the University of Connecticut disclosure form has to say:

Consider the implication of “State concisely what has been invented, i.e., what is to be offered to a company?” “What has been invented” and “what is to be offered to a company” are very different things. But here they are, conflated. For federal funding, “what has been invented” *is* what is offered to the federal government, at least by way of a nonexclusive license to practice and have practiced. We might note that UConn’s disclosure form provides no opportunity for an inventor to offer an invention to the public, or to the research community (including industry research), or to open innovation efforts. The required offer is to a single company, “a company.”

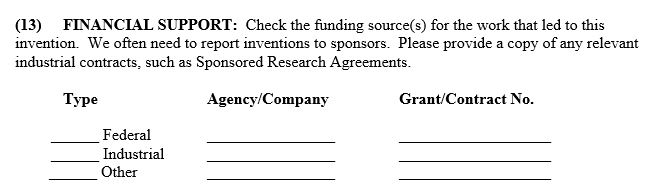

And here’s the disclosure form’s guidance for identifying sponsors of the invention:

“Funding source(s) for the work that led to this invention.” This description is ambiguous and incomplete. Work that led to an invention can be most anything. That could be work that showed that another approach was not viable. It could be work that was going off in another direction. It could be work for which the invention was a helpful tool utterly unspecified in any statement of work. Instead, what about the funding for the work from the moment of conception to reduction to practice? Even then, the money is not the point–the point is, what agreements have you made that would affect the disposition of this invention?

Of course, if the university has made agreements that affect the disposition of the invention, then how is it that the inventor (could be a graduate student, say) would have any knowledge of those agreements. Just because a graduate student receives a stipend (perhaps as a TA or an RA) does not mean that money has any bearing on the ownership of her invention.

One might put it this way: from what university accounts have you been paid while you worked on this invention? But that information is already available to university administrators. They can look it up. Why should an inventor have to chase down the information? From the account one can then look to see if there are any conditions on the funds involving the disposition of inventions. But even then there has to be a step to determine whether the invention that has been made is within scope of those conditions. Just because someone is paid from an account that carries conditions does not mean that the invention being reported has anything to do with the work carried out with money from that account. The invention could be closely related and yet not within scope. For instance, federal funds might be used to purchase a costly instrument, and that instrument might be used by another project to make some measurements that result in a patentable invention. Is the invention within scope? Should the inventor list the federal grant that acquired the instrument?

Furthermore, just because someone is paid from an account that does not carry any conditions with regard to inventions does not mean that a reported invention is not within scope of some research sponsor or licensee claim. One has to have not the source of money but the projects one is working on and the people involved and the nature of the relationship. It is the project that matters for federal reporting of subject inventions, not the money in an account–the “performance of work” . . . “funded in whole or in part by the Federal government.” What is the work? What agreements apply to that work? Is the reported invention within scope of any of those agreements?

For federal funding, the project may be limited to a specific grant or the project may be funded in part by that grant (in parallel with other funding, or at some earlier or later point in the project). An invention may be made outside a project that involves federal funding but which does not “distract or diminish” from the project–and is not a subject invention even though it is “closely related.” See 37 CFR 401.1 for the scope of federal claims on inventions.

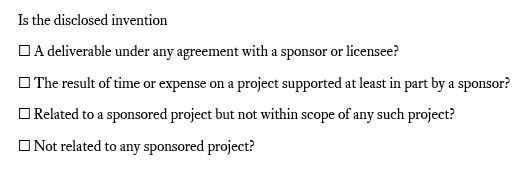

To get at the idea of project-agreement-scope-invention, we can sort things as follows:

(1) Deliverable. We committed to produce this invention for a sponsor or sponsors. It is a deliverable.

(2) Work product. This invention clearly results from work on this project, and the project has been supported by this sponsor (these sponsors). The sponsor(s) should have the benefit of this invention, even if not expressly requested. NASA calls such stuff “New Technology” and doesn’t care whether anything is patentable–report all you have done, made, created, gathered, discovered, built–whatever. Report it.

(3) Not in scope. This invention lies outside the planned and committed activities of any project supported by sponsors (or that carries commitments with external parties). We haven’t used project time or sponsor money to work on this invention, and working on this invention has not caused any change in doing our work on the project. The sponsor might be made aware of the invention for other reasons, but it is not something we proposed to do or the sponsor required us to deliver.

Not in scope inventions might be separated into “related” and “not related.” A “related” invention might involve the application of findings from a scientific project. The related invention is not in scope, but one would want to have written documentation to show that. An unrelated invention is generally evident on inspection. The funded project involved working with proteins; the invention involves a device for controlling temperature in lab refrigerators; not closely related.

If someone has grant funding based on their general expertise in a given field, and they invent something using that expertise, then it may take some work to document what was bargained for with a sponsor and what stands outside that agreement. It is neither a case that “everything” is committed to a sponsor “just in case” nor that an investigator can simply assert what is within scope and what isn’t. The whole point of a written agreement is to memorialize a meeting of minds on the matter.

Specifying deliverables is the essence of procurement contracts. Specifying whether those deliverables may depend on IP held back from the deal or unavailable from third parties is standard stuff. The challenge comes when the contract is to conduct research–explore–not to follow a specific protocol and deliver the results (as in a clinical trial, say). For that, one has to look to the “planned and committed activities” of the research project and ask whether a given invention arose in those activities. If so, then the invention is a work product of the grant-funded project and is subject to the invention requirements of the grant–even if the grant doesn’t fund all of the project and even if the invention wasn’t made with funds drawn from the grant account.

But universities generally copy each other’s disclosure forms, and figure if they are all rather alike, then they cannot possibly be all wrong. A look at UConn’s invention disclosure form shows how ambiguous it is. A list of grants for work that “led” to the invention doesn’t determine the university’s or inventor’s obligations. What’s necessary is a determination whether the invention is in scope for the obligations of any agreements. For that, one needs the statements of work.

We have four boxes then, for a general purpose disclosure form:

That would be a good start. One might then ask for the agreement identifier or at least the sponsor name–and the administrators could go pull the documents and verify the situation.

Rather than asking inventors to make judgments about funding sources, why not simply ask inventors to provide copies of the statements of work for all projects in which they have participated. Or better, don’t bother asking inventors to do one’s own clerical work. Ask the inventor for the earliest date on which they recognized they had an invention–conceived it or first actually reduced it to practice. Check all accounts on which an inventor has been paid from that time on and pull the associated job descriptions and statements of work/proposals/funding announcements associated with those accounts. The university already has that information–it doesn’t need to be disclosed by an inventor. Then go talk to the inventors. Then make a determination, as a matter of contract compliance, about what to report. Then document the determination and annotate the written record. Ah, but that would take actual work.